How to start a fashion label: Finance and Budgeting

How to start a fashion label: Finance and Budgeting

Your guide on how to build a sustainable and profitable fashion business if you’re not a nepo baby.

Welcome to another episode of the “Things I wish I knew before launching a clothing label” where I write in depth on how to start a successful international fashion business from the comfort zone of your computer. Today I’ll be writing about the most essential thing that no one tells you how to do and yet is crucial to master when it comes to running a business, aka “How To Budget”. Blah, I know, but one must do what one must do.

Now comes the not so fun part, especially if you’re a creative, this just might be a horror shitshow for you, just like it was for me. It’s the thing nobody teaches you and it’s a skill you simply have to have if you’re a business owner. The earlier you master it, the sooner you’ll get your affairs in order.

If you’re just starting out and reading this, your first thought will probably be “I don’t have to do this now. My KPIs are already on Shopify (or whatever the equivalent of this you’re using), I’m good. “ And while you’re probably right as far as the access goes, you’ll be wrong to assume that just because you’re a solopreneur for now and your business is not that complex, you don’t have to do the unnecessary stressful budgeting. Hate to be the bearer of bad news, but I’m here to tell you, don’t be an idiot or in a more polite manner please don’t be an idiot.

One of the mistakes I did early on is ignoring this aspect of the business. But you live, you learn and as someone who has lived for what almost feels like a century, I’ve deducted that stupidity can be avoided by learning how to budget while you’re in middle school. As someone who’s always hated this part of the business I’m honestly impressed as to how far I’ve come. So pay attention, as I’m showing you the ropes on how to get there faster and earlier than me.

I used to be one of those people who relied on Shopify, until I realized that regardless of how much the platform itself is made to help you, there are some things, it just can’t do for you, planning a budget being one of them. However, before we dive into the nitty gritty details of it, I’d like to bring your attention to processing payment systems.

PROCESSING PAYMENT SYSTEMS

If you want to work globally and process payments from the most common credit card issuers like Visa and Mastercard, you’ll need to add something known as a processing payment system to your online store. This has been quite the ordeal for me. Working from a country like Macedonia where Stripe and Paypal are not available, I had to get creative to resolve this issue, but that’s a story for another place and time.

For now what’s important to know is that if you’re working from the USA, Canada, any EU country member, any Scandinavian country and Australia, these commonly used processing systems will be available for you to use and it’s fairly easy to set them up. You can connect them directly from Shopify without needing any coding skills whatsoever. The most commonly used are Stripe and Paypal. Although Shopify offers a variety of alternative choices, these two are considered to be the best and most reliable ones.

If you’re a US citizen with a business registered in any of the 52 states, I highly recommend you use Shopify payments, as you’ll pay much less on processing fees. For some of us sadly this is not an option, so consider yourself lucky if you have it.

Other commonly used processing systems are Klarna and AfterPay and these are especially useful to offer as options, as they allow your customers to split payments in instalments while you get paid immediately.

Now that that’s sorted out, let’s move on to the next thing on the list, which is budgeting.

PLANNING A BUDGET

At the beggining of each year, I sit down with my own very hopeful thoughts and an Excell spreadsheet to craft up a budget for the year ahead. This usually consists of several things:

Fixed Expenses

Expected Revenues

Variable Expenses

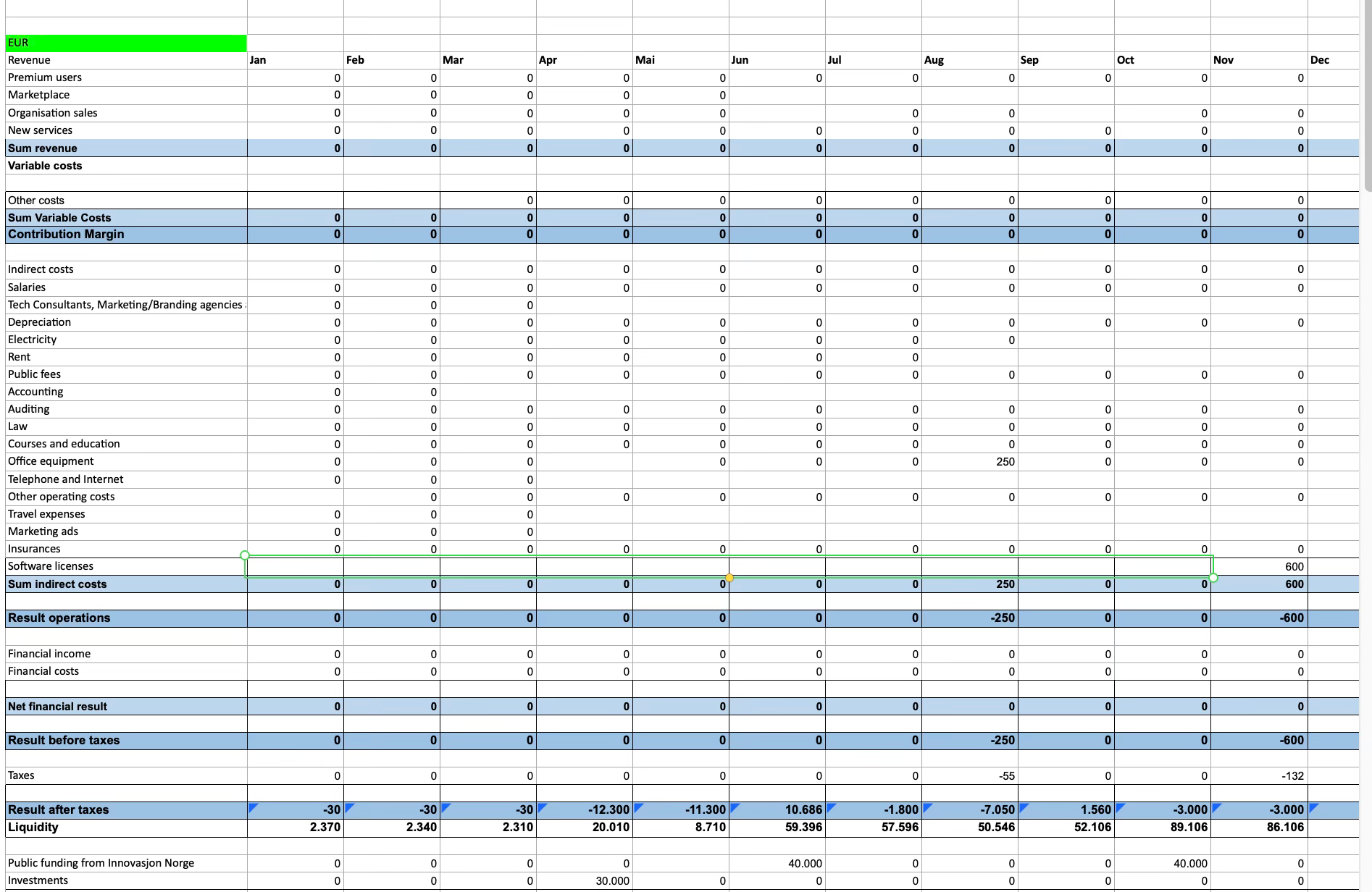

Let’s go step by step and define each of these. Fixed expenses include everything from salaries, utility bills, collection costs, marketing budget and every other cost you can think of which stays constant throughout the entire year.

Expected revenues is how much sales you need to make to cover the fixed costs and than added on top of that the desired revenue (enter a preferably realistic goal) based on previous year’s sales performance usually increased by 5%-10%. I always choose the pesimistic scenario, as it allows me to be pleasantly surprised at the end of each year.

Variable Expenses are those which change as the volume changes. Collaborator’s fees, commission fees, processing credit card fees are just some examples. These are usually calculated as percentage of expected sales. Stripe for instance charges different fees for processing different currencies, depending on where your company is registered and what’s your main currency.

While these numbers are not set in stone and oftentimes not even remotely accurate, planning will give you a general idea of what you can expect, for instance whether or not you’ll have enough money for a potential new hire and ultimately numbers will show if it’s realistic for you to achieve those goals. This will also impact your pricing strategy and expected volume.

Since I’m assuming that most of you are visual people, I’m including here a screenshot of the template I use. If you need this Excell spreadsheet, reach out and I’ll send it over.

CREATING SEPARATE BUDGETS

Now, here’s a thing I just only discovered not that long ago. If you want to maintain the liquidity of your company (that’s fancy financial term for having enough cash) so it can operate smoothly and not constantly lag behind with bills, one of the most important things to do is setting up separate checking accounts.

We use Mercury and here’s what that looks like for us. Each week when it’s time to do finance (for me that’s Wednesday), a certain amount is distributed from the main checking account to the sub accounts to make it easier for me to have an overview of just how much actual savings the company has at any given period.

When it’s all said and done, 10% of every transaction goes into savings which is then reinvested back into the business like purchasing fabrics or production budget for the next upcoming collection or marketing costs.

All the accounts are also directly linked to Xero, the online accounting system to enable us to automize the bookkeeping and ultimately make the whole process of tax filling easier for our accountant.

SETTING UP A PROFIT/LOSS SPREADSHIT

Back in 2015, I started wrting down every sale we generate, the profit it makes, where it’s ordered from, its size (for the purposes of keeping tabs on custom/regular size) and what type of payment has been used. It’s essentially a spreadsheet that keeps track of all of our sales divided my months. This gives us an overview of not just the number of sales, but how profitable a particular item is and automatically calculates the net profit/loss each month.

At the end of each year, this is analyzed and compared to the previous year, so that me and my team can have a better understanding of the state the business is in. Was it better, was it worse and what made it better or worse. As a creative person, I’m struggling to learn these figures by heart and I’m always having difficulties to give a straight answer to question like “ What’s your margin?”. Doing this enables me to give a confident answer to whoever asks, as I can look it up in a matter of seconds, which comes in handy especially when dealing with investors.

HOW TO FINANCE YOUR BUSINESS

While I started with the support of my family, my personal savings and a grant of 3.000EUR, I want to just quickly list down the options available to you, because back at the time I wasn’t even aware I had options to begin with.

THE 3F

The 3Fs stands for friends, family and fools. Unless you have a tech idea that’s promising to win the world over in a record period of time, your first call should be friends, family and an occasional clueless fool (if you can find one).

GRANTS

Grants are a debt-free source of funding to help you launch and grow your business. These are especially beneficial when you don’t have the 3F option. Here are few options you can check out for grant funding.

If you’re a woman, IFundWomen has a great database of available grants for women. They partner with corporate companies like Visa, Unilever, Diageo, Vista, Adidas, American Express and many more to deliver the best grants available for women.

The European Union has also grant programs that in addition to the EU countries support non-European countries based in Europe, called the Horizon countries like Ukraine, Macedonia, Albania, Bosnia and Herzegovina and Serbia. You can get more details on this on the European Union website.

Euro Nordic Funding Alliance is dedicated to empowering growth through strategic funding solutions, facilitating access to public funding for startups, SMEs, and associations across Europe and beyond. I met Niloufar, their founder while I was living in Norway. She’s an incredible entrepreneur herself with ambitious goals which I have no doubt she’ll reach one day. If you’re curious to find more, they’re organizing a summit this upcoming October in Stockholm which will gather an incredible rooster of entrepreneurs and impact investors. Tickets are already up for sale so if this is something you might be interested in, go ahead and book yourself one and I just might see you there.

CROWDFUNDING

Another source you could explore for funding is crowdfunding. Crowdfunding is a method of raising capital where numerous individuals contribute smaller amounts of their personal money to support a business.

If I’m being honest, we’ve never had luck with this one. Most of the platforms out there won’t give you access to their network, but it’s up to you to bring your own community on there, which if you ask me beats the purpose, since if you already have a community you can just go ahead and raise on your own and wouldn’t have to spend a dime on commission fees. However there are plenty who have found success using these platforms, so you can explore the concept at least. GoFundMe, IndieGoGo and Kickstarter are among the most popular ones and here’s a list of other popular crowdfunding platforms if you want to explore more.

As for the options connected to investing I won’t talk into too much detail, as I’m currently in the middle of raising myself, so I’m not sure what advice to share, as I haven’t mastered this yet. Once I do, I’ll put it in another article. For now, I’ll just list the available options to explore.

ACCELERATORS

Accelerators are a great place to apply for if you need help with your business plan and want to meet potential investors and even co-founders. Worth mentioning here are two which are a mix of venture capital and accelerator program, Antler and EWOR. Both of these provide venture capital (up to €150K), access to a network of over a dozen unicorn founders, and top-notch entrepreneurship education crafted by seasoned entrepreneurs making it easy for anyone who wants to be an entrepreneur to apply, get funded and build a strong network. Bear in mind though that neither of these invests in consumer focused companies, since apparently tech is all the rage these days. If you’re interested in exploring this in more details, I have a list of around 50 accelerators you can potentially use to apply, so don’t be shy and reach out.

ANGEL INVESTORS

An angel investor is an individual who provides capital to a business or businesses, including startups in exchange for convertible debt or ownership equity. My only advice here would be to sit down and make a list of all the potential investors and target those who have invested previously in your industry. Since my industry is fashion, I have compiled one with around 50 of my dream investors I’d like to have on my board one day. If you’re in the same industry, you can explore here angel investors who have invested in fashion.

VENTURE CAPITAL

Venture capital (VC) is generally a fund used to support startups and other businesses that have the potential for substantial and rapid growth and generally they don’t consider consumer companies to be among those, so you’ll rarely find one that invests in fashion. Even if you do happen to stumble upon one, like L Catterton which invested in Ganni, in order to get their attention, you’ll need to have made multimillion revenue first to just get yourself through the door.

I know it’s a lot to wrap your head around, but trust me, you’ll get there. My 2 cents here would be in order not to get overwhelmed by so many things that need to get done I suggest you pick a day when you’ll be doing just the finance and budgeting part of the business. Trust me it will help you focus better which will ultimately lead to increased productivity.

Well, that’s it folks. I hope this was usefull for all of you young aspiring fashion designers out there. Another part of this series is coming out next Sunday. Until then, because sharing is caring, if you know someone who is an independent fashion designer and will find this helpful please share it with them. I know I would have been grateful if I could find this stuff when I was beginning. It would have saved me a lot of time and money.

I know time these days is a precious currency, so thank you for reading.

Hasta la vista lovelies from my Salad Brain.

This is such a wonderful resource for founders!